Let’s be honest. Longer amortizations can make or break a deal. A 35- or 40-year term can mean the difference between qualifying for a home or being priced out completely. But while the monthly payment looks attractive, the long-term cost tells a different story. Here’s my reading:

The 50-Year Mortgage: A New Experiment in the U.S.

The U.S. housing market has been flirting with the idea of 50-year mortgage amortizations. The goal is simple: to make monthly payments more affordable in a market where home prices have outpaced income growth for decades.

At first glance, it sounds reasonable. Spread the loan over a longer period, and the monthly payment drops, allowing more buyers to qualify. But as a Toronto mortgage broker, I see both the temptation and the danger in that logic. We’ve seen this movie before. Longer amortizations, lower payments, but much higher long-term costs and slower equity growth. The difference is that here in Canada, we’re already seeing early signs of this with certain B lenders offering 35- and even 40-year amortizations on uninsured mortgages.

Extended Amortization In Canada

In Canada, the insured mortgage landscape is supported by three major insurers: CMHC, Sagen, and Canada Guaranty. Traditionally, insured mortgages were capped at 25 years, but first-time homebuyers can now qualify for insured mortgages with up to 30-year amortizations.

This update is significant for new buyers struggling to get into the market, particularly in major urban centers like Toronto and Vancouver. Beyond insured mortgages, some B lenders are currently offering 35- and even 40-year amortizations for uninsured mortgage products.

These extended terms can help borrowers who are:

- Self-employed with fluctuating income

- Carrying higher debt loads

- Buying or refinancing in high-priced regions

- Managing cash flow under elevated interest rate conditions

What a 50 Year Mortgage Really Means

If the U.S. moves forward with 50-year amortizations, a buyer could be paying for their home well into their 80s or 90s. While the monthly payment drops, the total interest cost skyrockets, often doubling compared to a standard 25- or 30-year term. Extending amortization doesn’t make real estate more affordable; it only spreads the debt over a longer horizon. The same logic applies in Canada.

A 35- or 40-year mortgage might reduce your monthly payment by 10 to 20 percent, but you could end up paying hundreds of thousands more in interest over the life of the loan. That’s a serious trade-off most borrowers don’t fully understand until they see the math.

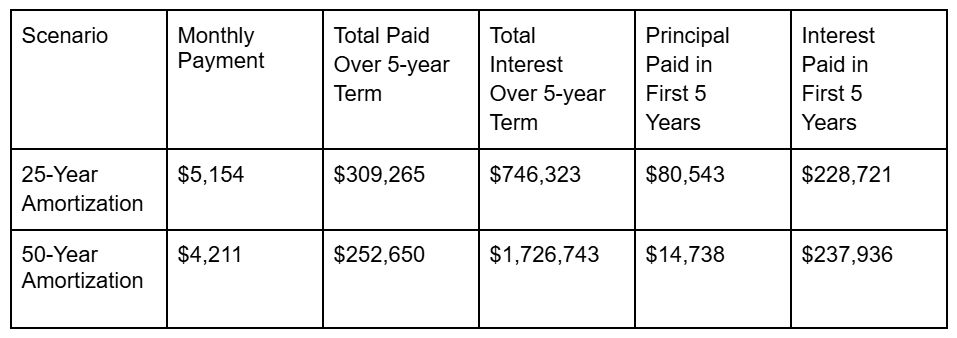

Numbers at a Glance: 25 vs 50 Years on a $1,000,000 Purchase

Assumptions: $200,000 down payment, $800,000 mortgage, 5-year term, 6% fixed interest rate, fixed monthly payments.

What This Means for Borrowers

The 50-year amortization trims the monthly payment by about $943 compared to the 25-year option. Over the full term, the 50-year structure costs roughly $980,000 more in total interest.

Equity builds much more slowly over 50 years. In the first five years, you’d reduce the principal by only $14,700 on the 50-year plan versus $80,500 on the 25-year plan. This huge gap occurs because the amortization formula allocates principal slowly with longer schedules. At the start, nearly all payments cover interest, not the actual loan amount.

Important Rate Note

In practice, mortgages with longer amortizations are often priced higher than standard terms, especially with alternative or B lenders. That means the real-world difference in total interest and equity growth can be even more dramatic than the illustration above. Rate premiums vary by lender, product type, and borrower profile, so I always price both options side by side and show the total borrowing cost, not just the monthly payment.

How U.S. and Canadian Approaches Differ

Both markets are struggling with affordability, but the regulatory frameworks are quite different:

In Canada, Toronto mortgage brokers play a crucial role in helping clients understand the full financial picture. We don’t just look at the lowest possible payment; we look at how each mortgage structure affects long-term goals, equity, and financial flexibility.

Why This Matters for Canadian Borrowers

If the U.S. normalizes 50-year amortizations, we could eventually see pressure in Canada to expand amortization limits further for uninsured mortgages.

That might sound like progress, but there are serious implications to consider:

1. It Can Push Home Prices Higher

When buyers can qualify for larger mortgages due to lower payments, it increases demand without solving supply issues.

2. It Slows Equity Growth

With longer terms, a greater portion of each payment goes to interest in the early years.

3. It Extends Debt Into Retirement

Many borrowers could find themselves still paying off mortgages into their 60s or 70s.

4. It Increases Total Borrowing Costs

Even with slightly lower rates from B lenders, the total interest over time becomes significant. As a mortgage broker in Toronto, I see extended amortizations as a temporary tool, not a permanent fix. They can provide breathing room, but they’re not a substitute for real affordability.

When Extended Amortization Can Make Sense

Extended amortization isn’t inherently bad when it’s used strategically. It can be a smart way to manage cash flow during uncertain periods or when planning for future income growth.

It can make sense when:

- A borrower expects income to increase in the coming years.

- A property generates positive rental cash flow, allowing leverage optimization.

- A self-employed client needs short-term payment relief while stabilizing business revenue.

However, these cases require a clear exit strategy. I often structure these longer amortizations as temporary measures with a plan to refinance or make lump-sum payments once the borrower’s financial position improves.

The Broker’s Role: Education Over Temptation

What concerns me most about the U.S. proposal isn’t the “50 years” itself, but the idea that affordability can be manufactured by stretching debt indefinitely. That’s where the role of a Toronto mortgage broker becomes so important. My responsibility isn’t to sell longer amortizations as the new normal. It’s to ensure borrowers understand the total cost of borrowing, not just the size of the monthly payment.

When I speak with clients considering longer terms, I ask three key questions:

1. What’s your long-term plan for this property?

2. How does this loan fit into your retirement or lifestyle goals?

3. Can you handle accelerated payments later without financial strain?

These questions shift the focus from “Can I afford the payment?” to “Does this mortgage

align with my financial future?”

Lessons from the U.S. for Canada

If the 50-year mortgage becomes mainstream in the U.S., it will spark conversations in Canada about further amortization extensions. But we should tread carefully. Longer amortizations may ease short-term pressure, but they can also inflate home prices, slow wealth building, and increase overall indebtedness. Rather than stretching loans to fit affordability, Canada should focus on improving housing supply, income growth, and targeted buyer support programs.

The 50-year mortgage proposal in the U.S. might make headlines, but it’s not a real solution to affordability. In Canada, we already have the flexibility of 30-year insured mortgages for first-time buyers and extended 35- to 40-year options through B lenders for uninsured borrowers.

Used wisely, these can provide temporary relief and open the door to homeownership. But as I remind my clients every day, the goal isn’t to find the lowest payment possible; it’s to achieve financial freedom sooner, not later. A mortgage should fit your life, not the other way around.

Alan Borcic is a Guest Contributor. Visit his website here.