Fixed vs. Variable Mortgages: Which Makes Sense In Today’s Climate?

How’s 2025 going for short-term real estate investors so far? Well, at this rate…

It depends on what path you’re on. Variable rates and fixed rates are in a state of flux. That means everyone’s bottom line currently rests on two things: their understanding of both options and ability to choose between them amidst economic change. Today, we’re going to take a short masterclass on how these financing arrangements work so you can make a smart decision for your bottom line.

The Fundamentals of Fixed Rates

Fixed rate interest is exactly what it sounds like – interest on a loan or investment that remains constant over time. The length of a term can vary but always consists of equally portioned installments. That remains true regardless of external economic conditions. With this type of loan, you’re essentially locking into an agreement with the bank to borrow money based on whatever rate they’re offering right now on a continuous basis.

Fixed rates are commonly sought after when looking for predictability in mortgages, personal loans, and other types of borrowing. For example, if a borrower gets a 5-year fixed-rate closed mortgage, the interest rate is locked in for 5 years, and the borrower pays a consistent rate during that period. After 5 years, the borrower can renew the mortgage at prevailing rates. This structure protects the borrower from fluctuations in market interest rates during the fixed term and helps with financial planning.

The Basics of Variable Rates

Variable rate interest is interest that changes periodically. Unlike a fixed rate, a variable rate can move up or down with market conditions, most commonly when central banks make updates to underlying benchmark interest rates or indexes. Lenders set variable rate offers for mortgages, credit cards, and other loans to that prime rate plus a set margin.

If the benchmark rate increases, the interest rate and corresponding payments will increase, and if the benchmark rate decreases, the payments will go down. While it means committing to a term of unpredictability, variable rates have the potential to pay off in long term savings when acquired at the right time.

It’s worth recognizing some variable arrangements can be ‘fixed’ with consistent installments throughout a term. What changes is the proportion of money going towards interest versus principal.

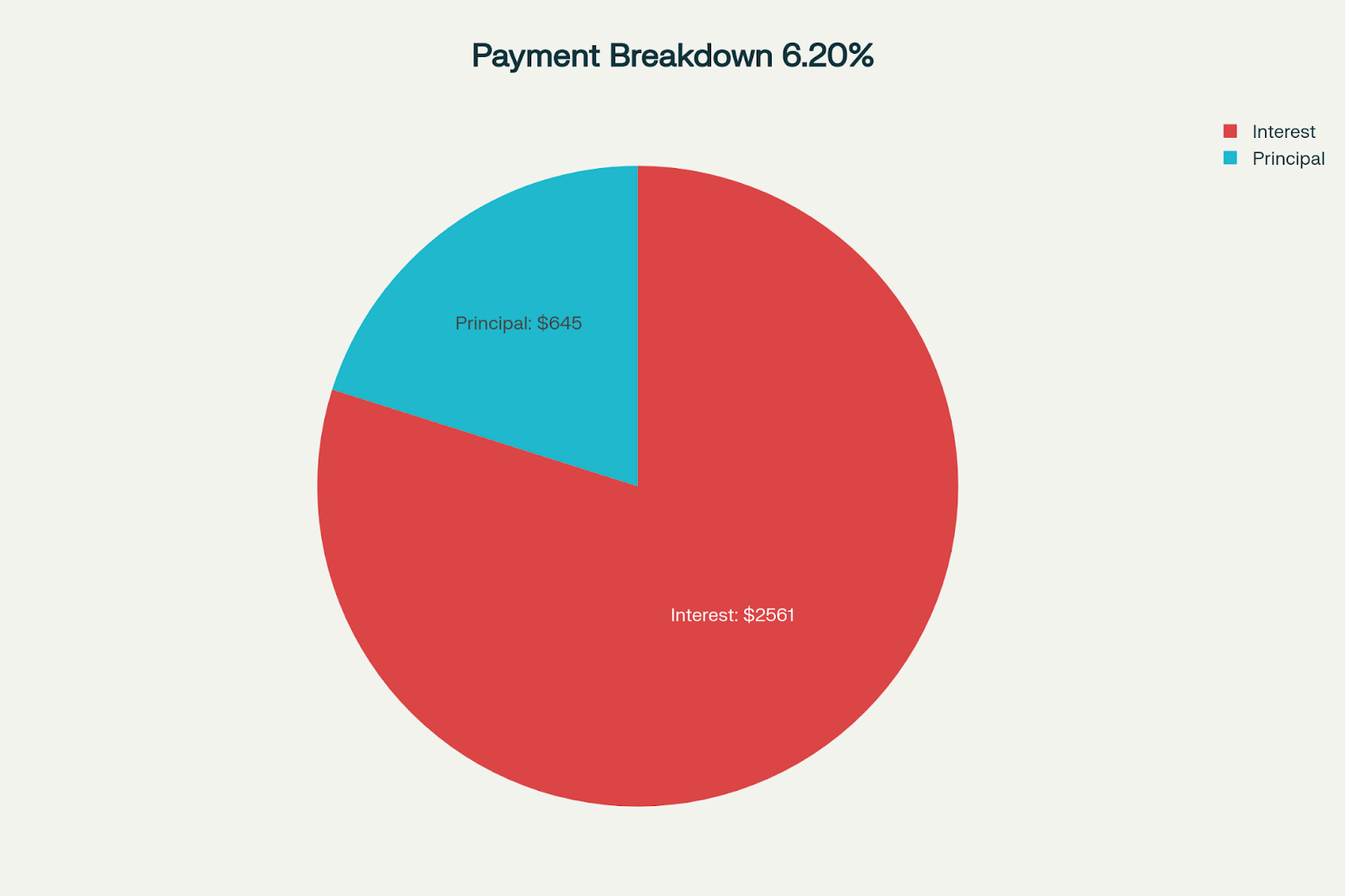

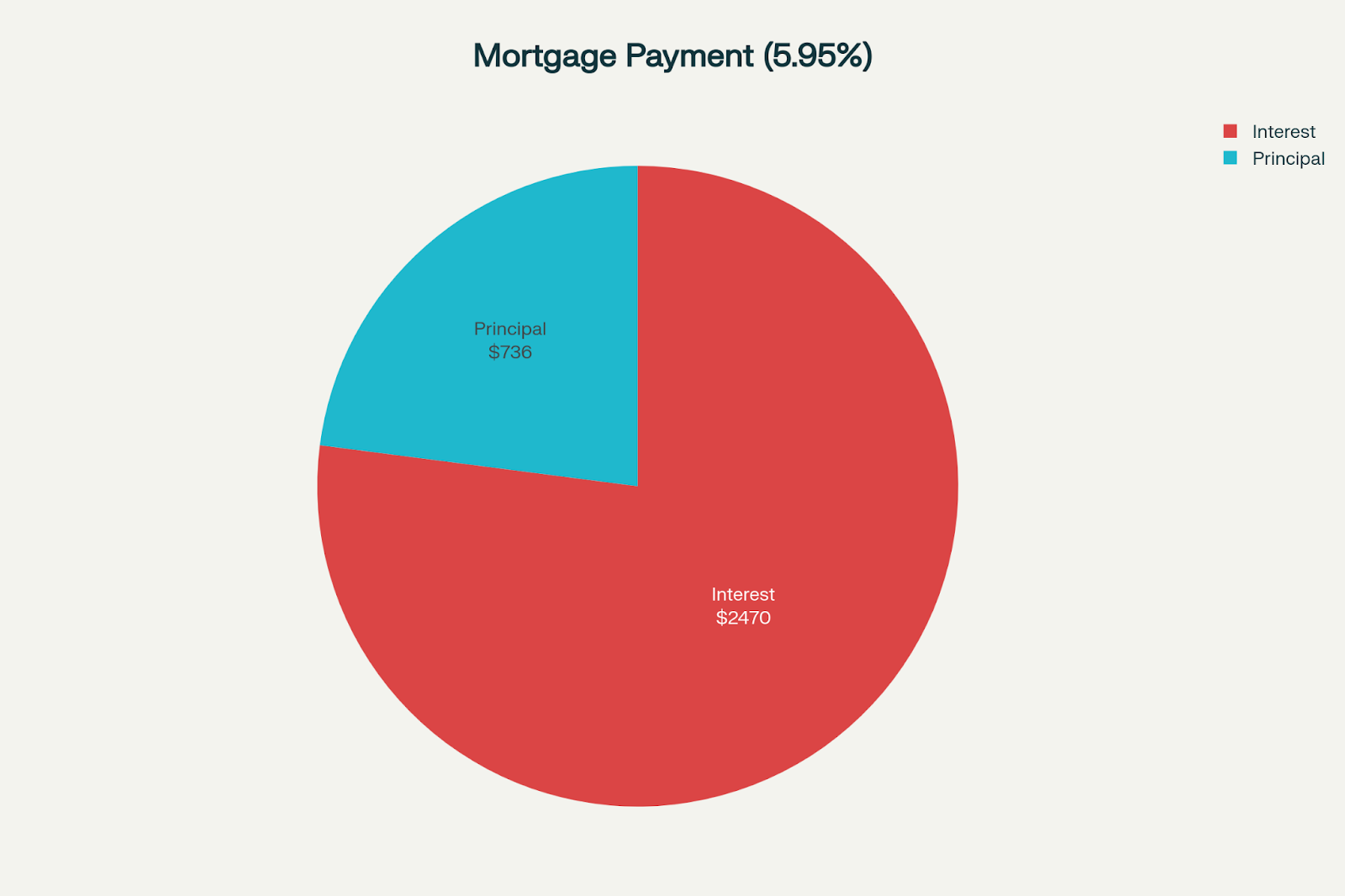

Suppose a borrower takes out a $500,000 mortgage on a 5-year variable term with a 25-year amortization, at an interest rate initially set at 5.95%. The monthly mortgage payment might be about $3,206, where $736 of that payment goes toward principal and $2,470 toward interest.

If after 6 months, the interest rate rises to 6.20%, the borrower still pays $3,206 monthly, but now approximately $2,561 goes toward interest and only $645 toward principal, meaning the mortgage is being paid down at a slower pace.

How Interest Rates Impact Your Rental Property Investment

As a mortgagee of short-term rental property, changes will affect you most directly because mortgage payments form a significant part of your monthly costs and cash flow.

Fixed-rates provide certainty through consistent payments that don’t fluctuate with market rates – making budgeting easier while protecting against sudden margin-reducing rate hikes.

A variable rate mortgage seems more cost-effective at surface level because it’s usually lower than fixed rate offers. But while they may start with lower rates and payments, payments – and carrying costs – may rise if central banks adjust rates upward to manage inflation or economic growth. Those higher mortgage payments could then reduce your profit margins or require raising rental prices, which might affect occupancy.

Is It the Right Time?

Variable and fixed rate interest wouldn’t both exist unless there was a sensible context for each. The challenge for real estate investors is knowing which option is best for their given circumstances. It’s why we see constant speculation about what Tiff Macklem or Jerome Powell have to say every few months; central bank updates serve as a bellwether for potential future rate cuts and increases.

To that end, there’s been a lot of discussion on both sides of the border lately. 2025 started with the Bank of Canada cutting its key interest rate several times, bringing it down from a peak of 5% in mid-2024 to around 2.75% by early 2025. This easing move was intended to support economic growth amid trade tensions with the United States and other uncertainties.

Meanwhile, the U.S. Federal Reserve maintained higher rates, with its policy rate hovering around 3.75%, reflecting a divergence in monetary policy approaches between the two countries.

The gap between Canadian and U.S. interest rates, expected to persist for some time, has significant implications for real estate investors. For Canadian mortgage holders, especially those with short-term rentals, lower Canadian rates might mean cheaper borrowing costs relative to previous years, spurring activity in domestic markets like Toronto.

As it stands, economists believe the Bank of Canada is likely to maintain its current key interest rate at 2.75% through the remainder of 2025. This pause follows several rate cuts that started in mid-2024, collectively dropping the rate by 225 basis points from earlier highs. The central bank’s cautious stance reflects a balancing act between supporting economic growth amid ongoing global trade uncertainties and managing persistent inflation that remains near their 2% target.

This all goes to show the importance of staying informed. The better you understand where rates are, where they’re going, and why, the better positioned you’ll be to make financing a short-term rental investment profitable for you.