Making money in the real estate business - or any business, for that matter - is a matter of mathematics. Especially with dealings in the multiple hundred thousands and sometimes million dollar range. All too many people get into short-term rentals thinking they're an easy means for passive cash when the reality is very different. There are tons of costs to consider, not to mention plenty of room for mistakes in arranging a mortgage. Go with the wrong interest rate or amortization schedule and you may find yourself losing money. We want to help prevent that with this masterclass on principal, interest, and managing monthly payments like a pro.

Mortgage Interest, Defined

Mortgage interest is the cost paid to a lender in exchange for borrowing the funds necessary to purchase a home. Every mortgage payment Canadian homeowners make includes an interest portion, which is calculated as a percentage of the remaining principal balance on the loan.

Canadian mortgage interest rates may be fixed—remaining constant for the length of the term - or variable, changing based on market rates.

For fixed-rate mortgages in Canada, interest is legally compounded semi-annually, meaning interest is calculated and added to the outstanding balance twice per year, even if payments are made monthly or biweekly.

Compounding makes the effective annual interest paid slightly higher than the nominal rate quoted on a mortgage. The interest portion of each payment is highest at the start of the mortgage and gradually decreases as the principal balance is paid down, so borrowers often pay more in interest than principal during the early years of their loan.

Mortgage Principal, Defined

Mortgage principal refers to the original amount borrowed to buy a property, excluding interest or other fees. For example, if a buyer puts $100,000 down on a $500,000 home, the mortgage principal is $400,000. Each regular mortgage payment is split between paying interest (the lender’s charge for borrowing) and paying down this principal balance.

Case Study: $500,000 Home in Canada

We've put together a sample case study illustrating the dynamic between interest and principal to show just how much it can sway a buyer’s rent-versus-own decision.

Consider a purchase price of $500,000 with a 20% down payment ($100,000). Qualifying for a 30-year amortization and a five-year fixed rate of 5.24%, the mortgage principal would be $400,000 and the monthly payment $2,192.

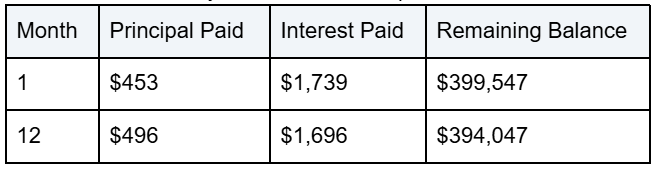

Sample Amortization Schedule: Where Does Your Payment Go?

Mortgage payment composition is dynamic. Cumulative contributions toward principal bring down the total amount to which interest is applied, thereby lowering borrowing costs. Where a majority of capital goes toward interest in the beginning, that changes over time at an accelerated pace.

Let’s look at the first year from our example:

The first 12 payments put $5,562 toward the principal and approximately $20,298 in interest. That means nearly 79% of total payments go to interest in year one.

For the entire 30-year period, If all payments were to be made as scheduled for the entire 30 year timeline, this mortgage would incur over $389,000 in interest (almost as much as the original principal) in addition to the price of the property itself to total $789,000. That's essentially 1:1 a ratio, where a dollar in interest is spent for every dollar to principal.

Why This Matters for Investors

With cleaning fees, insurance, and taxes to consider, it's easy to overlook or underappreciate the balance between mortgage principal and interest. But the consequences of doing so are costly. If a property doesn't appreciate fast enough or rental income doesn’t substantially exceed costs, much of an “investment” may simply enrich the lender.

Renting in lieu of purchasing can be financially smarter for the following reasons.

- Renters avoid interest drag and costly transaction fees.

- Funds that would have gone to interest can be invested or saved, potentially yielding greater long-term returns.

- Flexibility in relocating or adjusting housing needs is enhanced.

The Calculator That's Every Investor's Best Friend

Ratehub.ca’s calculator allows investors and aspiring homeowners to game out different scenarios. Use it to adjust down payment, amortization, and interest rates to see how much cost composition changes. You'll get a side-by-side comparison of the economics of renting vs. buying under given conditions. Projecting cash flow with a tool like this is crucial to confirming whether a property investment is truly profitable and worth your while.

Home ownership in Canada is often described as an investment, yet the reality revealed by mortgage math is more nuanced than most people expect. While building equity in a home can deliver long-term value, the high proportion of interest payments - particularly in the early years of a mortgage - can dramatically reduce the true financial benefit for many households.

Success in real estate begins not with optimism, but with mastery of the numbers. In the end, informed choices around interest, principal repayment, and overall housing costs is the smartest investment anyone can make when getting into this business.